Federal Reserve Expands Scope of Loan Options and Size of Eligible Businesses Under Main Street Lending Program

Hinshaw Alert | 7 min read

Jun 15, 2020

On June 8, 2020, the Federal Reserve Board (Board) announced an expansion of the scope and eligibility for its Main Street Lending Program. The Board also issued an updated FAQ for the program on June 9, 2020.

Under the three Facilities—the Main Street New Loan Facility (New Facility), the Main Street Priority Loan Facility (Priority Facility), and the Main Street Expanded Loan Facility (Expanded Facility)—the Federal Reserve Bank of Boston (Reserve Bank) will commit to lend to a single common special purpose vehicle (SPV) which will purchase participations in Eligible Loans issued by Eligible Lenders.

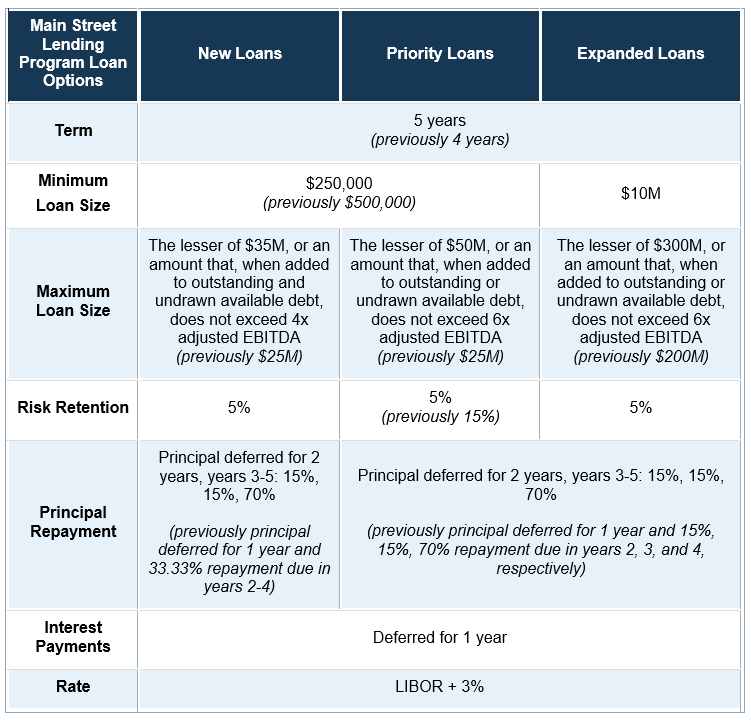

The Board expanded the loan options available to businesses and increased the maximum size of businesses eligible for support under the program. The changes include:

- lowering the minimum loan size for certain loans to $250,000 from $500,000;

- increasing the maximum loan size for all Facilities;

- increasing the term of each loan option to five years, from four years;

- extending the repayment period for all loans by delaying principal payments for two years, rather than one; and

- raising the Reserve Bank's participation to 95% for all loans.

The following table compares each of the options and their differences.

The Facility loans are full-recourse loans and not forgivable. As described in Section 4003(d)(3) of the CARES Act, the principal amount of a loan made through one of these three Facilities cannot be reduced through loan forgiveness.

A business may only participate in one of the three Facilities. If a business participates in one of the three Facilities, it cannot participate in the Board's Primary Market Corporate Credit Facility.

However, an Eligible Borrower may receive more than one loan under a single Facility, provided that the sum of New Facility loans does not exceed $35 million, or four times 2019 adjusted EBITDA; the sum of the Priority Facility loans received by a single borrower does not exceed $50 million, or six times 2019 adjusted EBITDA; and the sum of Expanded Facility upsized tranches received by a single borrower does not exceed $300 million, or six times 2019 adjusted EBITDA.

The Facilities are not yet operational. However, Eligible Lenders are being encouraged to begin funding Facility loans to borrowers in advance of the opening of the Facilities. Participations will be purchased in such loans so long as the required documentation is complete and properly executed, and evidences a loan consistent with the relevant Facility requirements. In addition, Eligible Lenders may also extend a Facility loan conditioned upon receiving a binding commitment that a participation in the loan will be purchased.

On May 8, 2020, Hinshaw published an extended discussion of the terms of the three new Facilities. The discussion below sets out the Eligible Loan Criteria of each Facility based upon the Board's expansion of the Main Street Lending Program. Unless indicated below, no other changes have been made to the terms of the program from our May 8, 2020 client alert.

1. Main Street New Loan Facility

Under the New Facility, the SPV will purchase 95% participations in Eligible Loans originated by Eligible Lenders after April 24, 2020. Eligible Lenders will retain 5% of each Eligible Loan.

Changes were made on June 8, 2020 to the Eligible Loan criteria for New Facility loans. The new criteria are set forth below.

Eligible Loans

An Eligible Loan is a secured or unsecured term loan made by an Eligible Lender to an Eligible Borrower that was originated after April 24, 2020, provided that the loan has all of the following features:

- Five-year maturity;

- principal payments deferred for two years and interest payments for one year (unpaid interest will be capitalized);

- adjustable rate of LIBOR (one or three month) + 300 basis points;

- principal amortization of 15% at the end of the third year, 15% at the end of the fourth year, and 70% at maturity at the end of the fifth year;

- minimum loan size of $250,000;

- maximum loan size that is the lesser of (i) $35 million, or (ii) an amount that, when added to the Eligible Borrower's existing outstanding and undrawn available debt, does not exceed four times the Eligible Borrower's adjusted 2019 earnings, before interest, taxes, depreciation, and amortization (EBITDA);

- is not, at the time of origination or at any time during the term of the Eligible Loan, contractually subordinated in terms of priority to any of the Eligible Borrower's other loans or debt instruments; and

- prepayment permitted without penalty.

2. Main Street Expanded Loan Facility

Under the Main Street Expanded Loan Facility (Expanded Facility), the SPV will purchase 95% participations in the upsized tranche of Eligible Loans from Eligible Lenders. Eligible Lenders will retain 5% of the upsized tranche of each Eligible Loan.

Changes were made on June 8, 2020 to the Eligible Loan criteria for Expanded Facility loans. The new criteria are set forth below.

Eligible Loans

An Eligible Loan is a secured or unsecured term loan or revolving credit Facility made by an Eligible Lender to an Eligible Borrower that was originated on or before April 24, 2020, and has a remaining maturity of at least 18 months—taking into account any adjustments made to the maturity of the loan after April 24, 2020, including at the time of upsizing—provided that the upsized tranche of the loan is a term loan that has all of the following:

- Five-year maturity;

- principal payments deferred for two years and interest deferred for one year (unpaid interest will be capitalized);

- adjustable rate of LIBOR (one or three month) + 300 basis points;

- principal amortization of 15% at the end of the third year, 15% at the end of the fourth year, and a balloon payment of 70% at maturity at the end of the fifth year;

- minimum loan size of $10 million;

- maximum loan size that is the lesser of (i) $300 million, or (ii) an amount that, when added to the Eligible Borrower's existing outstanding and undrawn available debt, does not exceed six times the Eligible Borrower's adjusted 2019 EBITDA (as defined above);

- at the time of upsizing and at all times the upsized tranche is outstanding, the upsized tranche is senior to or pari passu with, in terms of priority and security, the Eligible Borrower's other loans or debt instruments, other than mortgage debt; and

- prepayment permitted without

3. Main Street Priority Loan Facility

Under the Main Street Priority Loan Facility (Priority Facility), the SPV will purchase 95% participations in Eligible Loans from Eligible Lenders. Eligible Lenders will retain 5% of each Eligible Loan.

Changes were made on June 8, 2020 to the Eligible Loan criteria for Priority Facility loans. The new criteria are set forth below.

Eligible Loans

An Eligible Loan is a secured or unsecured term loan made by an Eligible Lender to an Eligible Borrower that was originated after April 24, 2020, provided that the loan has all of the following features:

- Five-year maturity;

- principal payments deferred for two years and interest payments deferred for one year (unpaid interest will be capitalized);

- adjustable rate of LIBOR (one or three month) + 300 basis points;

- principal amortization of 15% at the end of the third year, 15% at the end of the fourth year, and a balloon payment of 70% at maturity at the end of the fifth year;

- minimum loan size of $250,000;

- maximum loan size that is the lesser of (i) $50 million, or (ii) an amount that, when added to the Eligible Borrower's existing outstanding and undrawn available debt does not exceed six times the Eligible Borrower's adjusted 2019 EBITDA (as defined above);

- at the time of origination and at all times the Eligible Loan is outstanding, the Eligible Loan is senior to or pari passu with, in terms of priority and security, the Eligible Borrower's other loans or debt instruments, other than mortgage debt; and

- prepayment permitted without

FAQ

The updated FAQ includes the following guidance.

Affiliate Rules of Aggregation. The Small Business Administration's (SBA's) affiliate aggregation rules will be applied to calculate the business' number of employees and 2019 revenues for purposes of determining eligibility for Facility loans. An applicant must aggregate all of its employees and revenues together with all of the employees and revenues of "affiliated" businesses for purposes of determining whether the applicable employee or revenue caps are satisfied. "Affiliate" for this purpose is broadly defined in the SBA regulations (see 13 CFR 121.301(f)).

If a borrower is the only business in an affiliated group that has received funding through a Facility, the debt and EBITDA of the borrower, and not the entire group, is used to determine the maximum amount of the Facility loan. If the borrower's subsidiaries are consolidated into the borrower's financial statements, the consolidated debt and EBITDA must be used. If an affiliate of the borrower has previously borrowed or applied to borrow through a Facility, the entire affiliated group's debt and EBITDA will set the maximum loan size.

Holding Company and Operating Subsidiaries. If the borrower is a holding company, the Facility loan must be guaranteed on a joint and several basis by one or more operating subsidiaries. These subsidiaries must be eligible to borrow under the criteria of the Facility. The borrower will be required to provide adequate financial information with respect to such operating subsidiaries. In such circumstances, the EBITDA of any such subsidiaries must be used to calculate the borrower's maximum loan size.

PPP Loans and Economic Injury Disaster Loans. A business cannot participate in a Main Street Program if it has received "specific support" under Subtitle A of Title IV of the CARES Act. Funds provided under the CARES Act to specific industries, such as airlines or entities participating in the Primary Market Corporate Credit Facility, both constitute "specific support" that bars participation in a Main Street Program. Recipients of PPP loans can participate in one of the three Facilities. Borrowers that received Economic Injury Disaster Loans are deemed not to have received "specific support" as defined in the CARES Act and, therefore, may participate in one of the three Facilities.

Non-Profits. Nonprofit organizations are not currently eligible to participate in the Main Street Programs. The Board is "working to establish soon one or more loan options that are suitable for" nonprofits.

Unforgiven Portion of PPP Loans. The outstanding unforgiven portion of a PPP loan counts as outstanding debt when calculating the maximum amount of a loan.

Related People

Related Capabilities

Featured Insights

Employment Law Observer

Aug 10, 2026

As Leaves Fall, Leave Requests Rise: Are You Compliant With Chicago’s Expanded Rules?

Press Release

Aug 7, 2026

Daniel McGrath Re-Elected Senior Director of the Federation of Defense & Corporate Counsel

Insights for Insurers Alert

Aug 7, 2026

California Supreme Court Clarifies Pleading Standards for Excess Policy Claims

Employment Law Observer

Aug 10, 2026

As Leaves Fall, Leave Requests Rise: Are You Compliant With Chicago’s Expanded Rules?

Press Release

Aug 7, 2026

Daniel McGrath Re-Elected Senior Director of the Federation of Defense & Corporate Counsel

Insights for Insurers Alert

Aug 7, 2026

California Supreme Court Clarifies Pleading Standards for Excess Policy Claims

Press Release

Aug 6, 2026

Charles Townsend Named a Best Mentor Finalist in the 2026 ALM Texas Legal Awards

Webinar

Aug 5, 2026

April Toy Moderates HNBA Webinar on AI in the Practice of Law

Privacy, Cyber & AI Decoded Alert

Aug 5, 2026

2026 AI Compliance: Upcoming Laws Every Organization Needs to Know

Press Release

July 21, 2026 | Updated on August 4, 2026

Three Hinshaw Attorneys Named to the 2026 National Black Lawyers’ Top 40 Under 40 List

Healthcare Alert

Aug 3, 2026

Fixing the Emergency Refill Trap: What California’s AB 1587 Means for Pharmacies

Consumer Crossroads: Where Financial Services and Litigation Intersect

Jul 30, 2026

Should Text Messages be Considered “Calls” Under the TCPA? The Seventh Circuit Says No

Healthcare Alert

Jul 30, 2026

California Courts Sharply Curtail the MICRA Damages Cap in Nursing Home Litigation

Insights for Insurers Alert

Jul 30, 2026

Analyzing a Couple of Cases Involving Exclusions in D&O Policies

In The News

Jul 29, 2026

Hinshaw Authors Contribute Two Articles in Latest Edition of the CCFL Quarterly Report